2024 Bad Bot Report Explore the latest trends & impact of unmanaged bot traffic

Get the report

Comprehensive digital security

Imperva latest news

KuppingerCole Report: Why Your Organization Needs Data-Centric Security

Read more

Data Security in 2024: Unveiling Strategies Against AI-Driven Cyber Threats

Watch webinarThales & Imperva join forces to create a global leader in cybersecurity

Find out moreEnterprises move to Imperva for

world class security

Faster response

Accelerate containment with 3-second DDoS mitigation and same day blocking of zero-days.

Deeper protection

Secure applications and data deployed anywhere with positive security models.

Consolidated security

Consolidate security point products for detection, investigation, and management under one platform.

Imperva products are quite exceptional

Protecting modern web applications

Enterprises need security at multiple layers to effectively protect against different types of attacks and reduce risk.

Learn more

Assure data compliance and privacy

Streamline processes and know what data you have, where it is stored, how it is handled, and by whom.

Learn more

Prevent account takeover fraud

Have confidence that your web applications are protected against today’s automated account fraud.

Learn more

Stop software supply chain attacks

Gain control of risky behaviors between custom and third-party application components.

Learn more

Mitigate malicious data activity

Protect against malicious data access to defend the end of the attack chain as XDR solutions cannot.

Learn more

Automate insider threat management

Use continuous visibility and automation to shut down high-risk privileged data access.

Learn more

Ensure consistent application availability

Automatically optimize and protect at the edge to minimize the likelihood of downtime with zero performance impact.

Learn more

Embed security into DevOps

Provide developers with the tools they need to adopt the latest technology and prove it’s safe for management.

Learn more

Securely move your data to the cloud

Grow beyond compliance monitoring to secure cloud data with minimal disruption to users during transition.

Learn moreRecognized leadership

API Security & Management Overall Leader

Imperva named an Overall Leader in the 2023 KuppingerCole Leadership Compass for API Security & Management

Read the report

Read the report

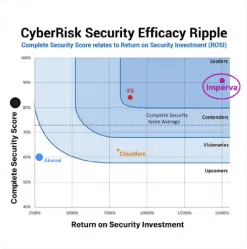

Imperva named a security leader in the SecureIQLab CyberRisk Report

2022 Cloud Web Application Firewall (WAF) CyberRisk Validation Comparative Report

Read the report

Read the report

Data Security Platform Overall Leader

Imperva named an overall leader in the 2023 KuppingerCole Leadership Compass for Data Security Platforms

Read the report

Read the report

Recognized as a market, product, and innovation leader

Imperva named an overall leader in the 2022 KuppingerCole Leadership Compass for Web Application Firewalls

Read the report

Read the report

Delivers DDoS protection in an application suite

The Forrester Wave™: DDoS Mitigation Solutions, Q1 2021

Read the report

Read the report

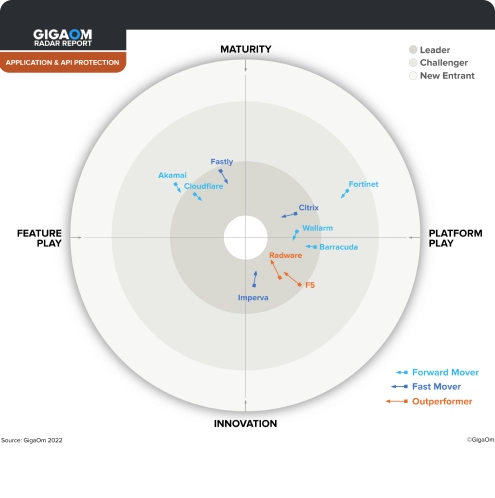

Expansive Web Application and API Protection

Imperva named a Fast Mover and Innovator in GigaOm Radar for Application and API Protection

Read the report

Read the report